Historical View, 1990-2024 Sensex vs Gold vs PPF - I

With the limited Indian capital market data (1990 onwards), we try different asset allocation combinations for SENSEX, PPF and Gold to get see what works best for a 30 year retirement plan. The outcomes were a revelation.

Aseem Sharma

6/28/20243 min read

I’ve discussed various ingredients of Retirement Planning in my previous posts. I think it’s time we applied some of the concepts to Retirement Planning in the Indian Context and look for ourselves where things stand.

For the purpose of this post, let me first summarise the scenario and the data.

Scenario

We consider investments across 3 asset classes. Equities (SENSEX), Fixed Income (PPF) and Gold.

The period under consideration is Jan-1990 to May-2024. Like in the 4% rule discussion, we are considering a 30 year retirement period. We construct 54 Retirement Paths. Starting Jan-1990 to Jan-2020 and ending May-1994 to May-2024. I know the data is limited but I promise you its Insightful as we will see in a bit.

It’s a simplified representation in the sense that there is no emergency corpus or taxation considered.

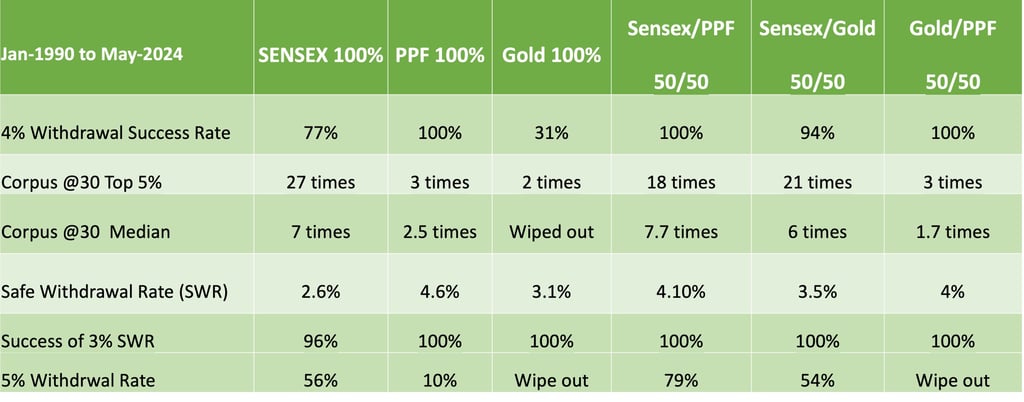

We consider 6 investment scenarios for the captured period.

100% in SENSEX

100% in PPF

100% in Gold

SENSEX-PPF 50-50

SENSEX-Gold 50-50

Gold-PPF 50-50

For withdrawal rates, we start off with 4%. We then consider 3% and 5%. Finally, we find out what’s the Max Safe Withdrawal Rate for each of the scenarios (i.e. we exhaust the corpus exactly at the end of 30 years).

The Data and its Source

Sensex Monthly Values from 1990 to May-2024 from Market watch

Gold Monthly Values in USD Investing.com

INR to USD rates 1990 to May-2024 Investing.com

PPF Historical Rates 1990 to May-2024 dailytools.in

Inflation Data 1990 to 2024 macrotrends.net

Insights

We have a wide range of outcomes as we apply different lenses. Refer to the table published. The things that stood out to me were…

How PPF alone stood the test of time and delivered 100% success for a 4% withdrawal for a 30 year timeline. I was not expecting that when I started compiling the data. After all, Sensex has delivered a stellar 14% return from 1990 to 2024 “On an Average”. PPF delivered the goods for not just 30 years, but if one were to outlive the 30 year period, the corpus could last for upto more 5 years. It can’t be demonstrated with the present data set as we haven’t got a single 35 year Retirement Path, but from what at the end of the 30 year periods, we still had 2x corpus in our kitty. With that I believe we could push another 5 years. But then remember, as taxation isn’t considered we need to temper our enthusiasm.

Gold by itself, performed the worst. But when combined with Sensex the combo did better than either of them in isolation. This is the benefit of diversification. I describe it in more detail {here}.

While PPF could deliver a 4% or even push a 4.6% Max Safe Withdrawal Rates for 30 year retirement timeline, it could never scale beyond 4.6%. See, how at 5% Withdrawal Rate the success dips to mere 10% way below SENSEX's 56%

The most effective in my view was a combination of PPF and SENSEX. While it delivered 94% success for a 50-50 split, it could not survive the Harshad Mehta euphoria of April and May ’92. If we however change the investment ratio to 67% PPF and 33% SENSEX, it not only survives Harshad scandal but still delivers 58% success with 5% Withdrawal Rate.

The variability of the outcomes is also stunning. For SENSEX/Gold combo one is as likely to run out of money as one is to end up with 21 times the original corpus allowing for 8%+ Withdrawal Rate for the entire 30 year period.

We could also see a Safe Withdrawal Rate SWR of 3.5% and above for combo asset allocations reinforcing diversification.

In the end, the data proves the age old axiom that in retirement, the asset allocation should lean in favour of fixed income.

Disclaimer : I'm NOT a SEBI Registered Investment Advisor or Analyst. All content on this website is for educational purpose only. Consult your financial advisor before making any financial decision including investing.