Charming and Temperamental Ms. Volatility and The Myth of Average Returns!

How Volatility impacts the financial outcomes for Retirees. Why going by CAGR and Average Returns can be misleading

Aseem Sharma

6/23/20245 min read

In my earlier post, I introduced Mr. Compounding, the fellow Yatri in your Retirement Yatra. In this post let me introduce you to the charming and temperamental Ms. Volatility, another fellow Yatri eager to hitch a ride with you. However, unlike Mr. Compounding who vows “Till Death Do us Part”, association with Ms. Volatility is entirely voluntary, based on your personal discretion. Her services are listed in a glossy brochure called “Wonders of Compounding” showing off mouth watering Annual “Average Returns”, and stellar “CAGR”. Hidden away in the fine print is the statutory warning, if you choose to notice, cautioning you to the perils of Volatility. “All investments are subject to market risk. Read scheme related document carefully before investing!”… Yada, yada! Essentially, anyone selling you investment in Equities, Gold, Bonds, Crypto etc. is doing Ms. Volatility’s bidding. Yes, even bonds are susceptible to interest rate risks as so many bond investors found out post 2022 treasury yield surge.

Just like Mr. Compounding, Ms. Volatility charms you during your earning years. The outsized ROI you made on your investments during these years were mostly her blessings delivered by Mr. Compounding but only if you survived the gut wrenching market gyrations, you weathered market corrections that over the years tested your resolve. The palpitations you felt during those bear markets are part of the same “Average Returns” package deal with temperamental Ms. Volatility. How to deal with her during her violent mood swings remains a subject of much debate. One such strategy is to time the market. Traders’ graveyard is littered with unmarked graves of the “Trader Matadors” who got trampled by Ms. Volatility trying to Time the Market. The other less lethal option is doing SIPs. While SIP may not offer "bumper to bumper" protection, they do often help soften the blows. But what really gives us strength during these dark periods is the fact that we are still in our earning years and do not need to withdraw from our corpus during the tumultuous times.

As with Mr. Compounding, our relationship with Ms. Volatility undergoes a tectonic shift the day we Retire. With an equity heavy portfolio and no SIP to smoothen things over, we are better off scaling back our relation with Ms. Volatility in favour of the Conservative Curve. If you have a sizeable corpus, you may move most of the portfolio in low volatility investments locking in the cashflows early on in the retirement yatra. Most of us do just that lest our portfolio be susceptible to “Portfolio Failure”. “Portfolio Failure” a term I first examined in my post on Retirement Curves is used to describe retirees running out of money in their lifetime due any of the underlying assumptions regarding Retirement Planning going wrong. We had kept the discussion on volatility in abeyance back then. We pick it up right here.

A conservative portfolio’s ROI tracks to inflation as all the investments are in low volatility, low returns instruments. It rarely beats inflation and underperforms a lot. Due to low ROI, conservative portfolio has has shorter timelines. In order to extend the timeline, we need to re-enrol Ms. Volatility by investing a part of the corpus in equities, gold, etc. As we saw bumping up the ROI by just 2% above inflation extends our corpus from 35 years to 60. We also touched upon the trade off needed i.e. accept higher risk of Portfolio Failure for a longer runway.

Assets with variable returns improve "average" performance while increasing the probability of extreme outcomes.

The Myth of Averages

Let’s understand the world of averages with another example. Imagine a scenario where you wish to cross a river on foot but you do not know how deep it is. You ask someone the question and he replies that the average depth is just 3 feet. Based on the information, should you attempt to wade through the river? Perhaps not. Riverbeds have variable depths . “Average” does not reveal that the river may be 12 feet deep around the centre and shallow in most other parts. Similarly, the fact that the Sensex gave 16% return every year “on an average” since inception (1979), does not reveal the fact that there was a 10 year stretch during the last 45 years where the Sensex was down ~20% (Rs. 100 invested was down to Rs. 80, 10 years later)

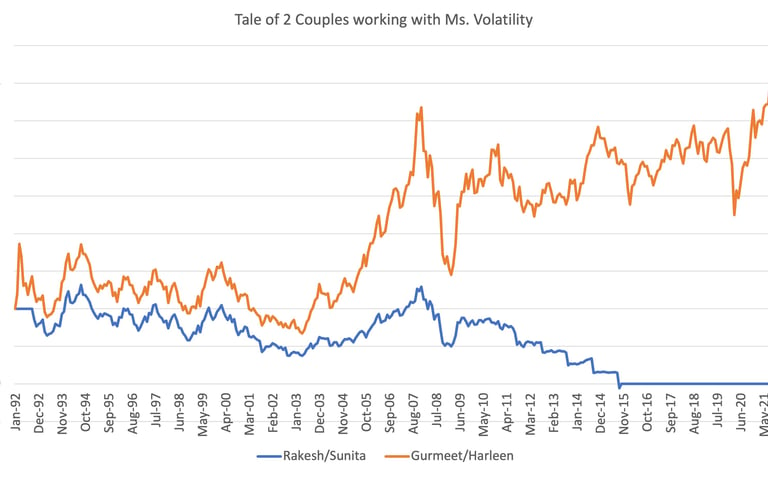

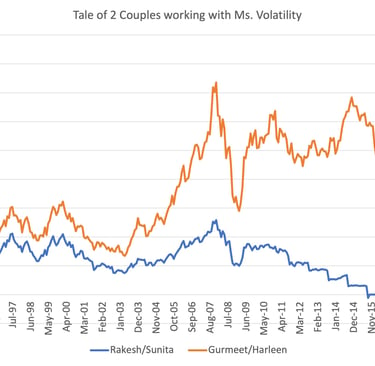

Let’s apply the above learning to a hypothetical retirement couple. Rakesh and Sunita, started their Retirement Yatra around 30 years ago in Oct ’92 with a Rs.30 lac corpus. They planned for a 30 year retirement and put all their investments in Sensex(Index Fund). When starting off, they planned for annual withdrawal rate of 4%. i.e Rs. 1.2 lac per year or Rs. 10,000 per month. This withdrawal amount would increase every year based on inflation. To clarify, irrespective of the value of their portfolio the next year, year after or any year thereafter, Rakesh and Sunita would withdraw equivalent of Rs. 1.2 lac adjusted for inflation every year.

Looking up historic data, we see that Sensex was around ~2,800 in Oct ’92 and ~61,000 in Oct ’22. That gives us ~10.7% “average” annual growth rate over 30 years. The inflation during the same period was ~7%. We clearly see that “On Average” Rakesh and Sunita earned 3.7% higher (10.7% -7%) than inflation every year. Going by the “averages”, their Corpus should should last more than 60 years. Refer to the withdrawal rates and timelines.

Reality Check! They ran out of money as early as Oct ’15, a good 7 years before the planned 30 years. For that matter, if they had retired with a Sensex only portfolio anytime between March ’92 to Mar’93 or Jan ’94 to Jun ’94 they would have exhausted their corpus before 30 years. Now that’s really scary!! What do we attribute this failure to? The downturns of Harshad Mehta scandal, ’97 East Asian crises, Dot Com bust in 2000, Ketan Parekh scam, 9/11, 2008 crisis and the taper tantrum all played their part.

You may wonder if was it even possible to survive these 30 years with a 4% withdrawal rate without investing in equities(Sensex)? The answer to that is “Yes”. And it’s a revelation. If only, Rakesh and Sunita had invested all their corpus in PPF or instruments paying equivalent returns year on year, they would have safely navigated all the crises listed above.

While above is a gloom and doom cautionary tale, imagine another couple Gurmeet and Harleen who retired the same year with the same corpus in Feb ’92(Sensex 2,700) and put their Rs. 30 lacs in Sensex. They not only happily navigated the 30 years to Feb ’22(Sensex 56,000) with the CAGR of ~10.57% (less than 10.7% in the previous case), but were still be left with a respectable Rs. 1.1 Cr Corpus (3.7 times original corpus of Rs. 30Lacs). All that after withdrawing 4% of the original corpus adjusted to inflation every year for 30 years.

Both couples invested in SENSEX, ran through mostly overlapping period just 10 months apart starting with same corpus, expenses and inflation. Sensex ROI for both the couples was CAGR of ~10.6%. Reading the “Average Returns, CAGR” Brochure both the couples would be smug in their belief that they are in the Perpetual Corpus bracket. Above all, they both entrusted their financial fate in the hands of Charming and Temperamental Ms. Volatility. They believed in the myth of “Average Returns”

Disclaimer : I'm NOT a SEBI Registered Investment Advisor or Analyst. All content on this website is for educational purpose only. Consult your financial advisor before making any financial decision including investing.