Life Expectancy at Birth vs at Retirement

Longevity is the most crucial variable when planning for retirement. Its the great unknown. The right metric to use for planning is Life Expectancy at Retirement and Not the commonly used Avg. Life Expectancy at Birth.

Aseem Sharma

6/17/20243 min read

Compounding’s most powerful ingredient is time. For a Retiree, Time is “Life Expectancy” (LE). Retirees' biggest fear is what if they outlive their corpus. In the Retirement Planning equation , LE is the biggest unknown. How long should one plan for?

In one of my previous posts, Retirement Curves, 2 of the 3 curves are time sensitive. Especially, if all of one’s investments are in secure low -risk instruments, there is a certainty that the corpus will run out by the end of the planned period. Retiree is forewarned to ensure he chooses a time period with enough headroom. But even then, how much is enough? Is there even a way to definitively predict the number of years one must plan for post retirement?

70 is the most thrown around number I hear from Retirement Planners regarding Life Expectancy(LE) for Indians. Based on a Mint article* The same LE was 35 years in 1950, and will likely rise to 82 years by 2100. LE is clearly on the rise and given emerging information, may lie between 70 and 82 for more recent retirees. However, 70 is life expectancy at birth and is completely different from life expectancy at retirement. The LE commonly discussed in the former but latter is the right measure when planning for retirement.

There is an entire field of probability called “Conditional Probability” which aims to determine probability of an outcome “A” given event “B”. To frame this in terms of Retirement Planning, what’s the LE of a person at the retirement age of let’s say 60? It’s a very different question from asking what’s the LE at birth which includes child mortality in its calculations. What we should really be asking instead is how much longer is a person expected to live once she has crossed 60 — the standard retirement age in India. And that number is greater than LE at birth(70).

I searched around for more information to determine LE at Retirement for India. Unfortunately, there’s limited literature available out there. I found a document published by Limra** and If we go by that document, for India the LE at 60 is 18+ years and likely to grow to ~20 years by 2050. (Refer to page 17 Figure 8). Clearly this adds 8 golden years to the initially estimated LE at birth of 70 years and therefore would mean greater expenses plus inflation, hence would require a bigger corpus.

But even LE at 60 is not enough, Life Expectancy is just a midpoint. 50% people are likely to live beyond. We need know what’s the 80th or 90th percentile or even the 95th percentile to plan our Retirement as none of us would want to be short of funds when we are 93. The life insurance business run by the Actuaries is predicated on answering this vital question at various life stages for varying health conditions, gender, habits etc. They have the answer but I could not find this information for India in public domain.

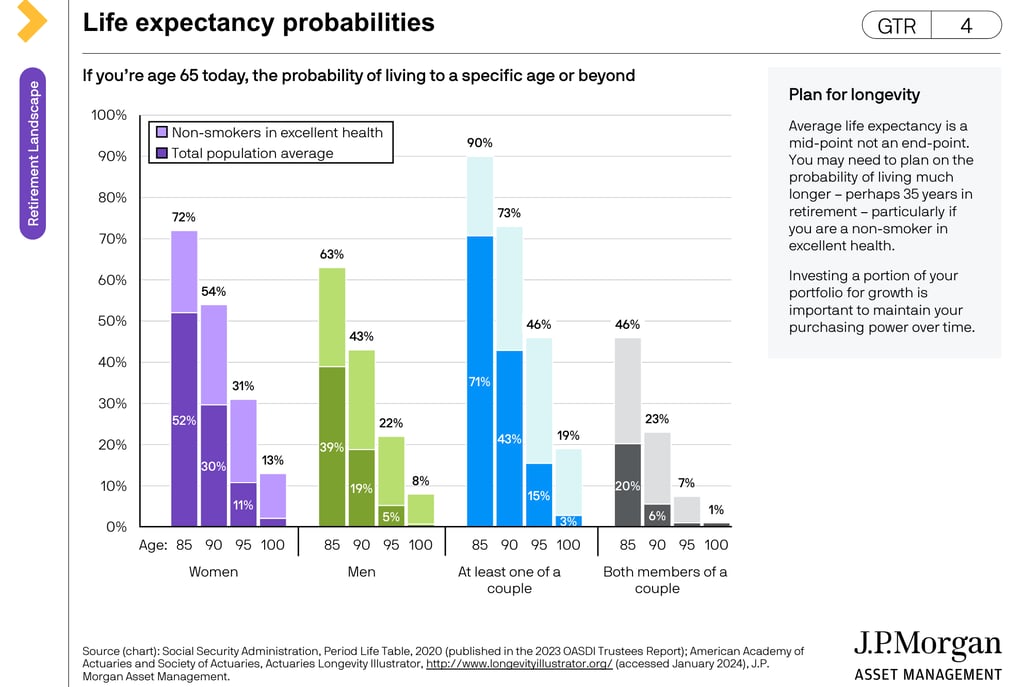

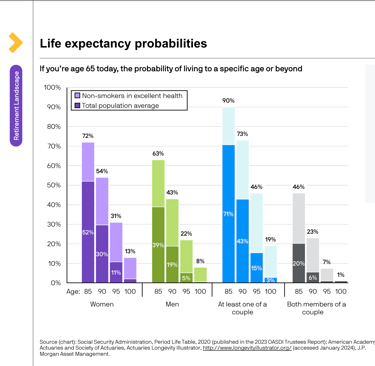

And so, I’m going to refer to another document I discovered. It’s published by JP Morgan Asset Mgt.*** for the US demography and they have done some really insightful study. I wish we had something like this for India. Their study points out that If both the partners are in great health at 65, there is 1 in 5 chance that one of them will live past 100. JPMC are recommending to plan for 100 years of LE at 65 (Retirement age in the US).

Honestly, the document scared the living daylights out of me. I can’t over emphasize enough the role of LE in Retirement Planning. Especially for low-risk portfolio holders this study could have significant(catastrophic) implications if they are planning for typical 25 years at 60. Given the age gap between Indian couples(women are 4-5 years younger) and the fact that women have higher LE than men, it makes sense to plan for longer retirement periods. I recommend people interested in Retirement Planning read this report. It has some great insights. Even when you ignore US tax planning part, there is a lot of information that could help us plan better for our retirement here in India.

References

* Mint Article on Life Expectancy https://www.livemint.com/news/india/indias-life-expectancy-to-hit-82-by-2100-as-per-un-estimates-11665298822775.html

** Limra Article on Life Expectancy at 60 https://www.soa.org/globalassets/assets/Files/resources/research-report/2018/2018-retirement-spotlight-india.pdf

*** JP Morgan Asset Mgt presentation on US Life Expectancy https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/retirement-insights/guide-to-retirement-us.pdf

Disclaimer : I'm NOT a SEBI Registered Investment Advisor or Analyst. All content on this website is for educational purpose only. Consult your financial advisor before making any financial decision including investing.