1990-2024 Sequence of Returns Risk - IV

How Sequence of Returns threaten your retirement plan. What can one do to mitigate the Sequence of Returns risk.

Aseem Sharma

7/4/20244 min read

So far in this series we covered various factors that impact Retirement Planning. We covered, impact of Volatility, Optimal Asset Allocation, Safe Withdrawal Rates for different timeframes, the benefits of dynamic withdrawal plans, diversification etc. One factor we briefly touched upon, but did not spend much time dwelling on was “Sequence of Returns”, (SOR). In this post we cover SOR in a bit more detail. I mentioned in the 4% rule post, that retirees are especially vulnerable to negative returns in their initial years of retirement. On the other hand, if they bag a couple of good years of returns at the start of their Retirement Yatra, they build up a natural buffer (immunity) to future market shocks.

SOR is a close cousin of Ms. Volatility. She could bless or doom a retirement plan in the first couple of years. The blessed dream walk through their retirement without ever realizing they were blessed. But for the cursed, the bleeding from the whiplash takes years to heal, inflicting a lifetime of agonising financial pain.

When investing in the market, we experience both positive and negative returns. Supposing we stay invested during the crests and troughs of the markets(not withdraw), it would not matter what sequence these returns follow. Whatever the sequence, we would end up that the same place at the end of the period.

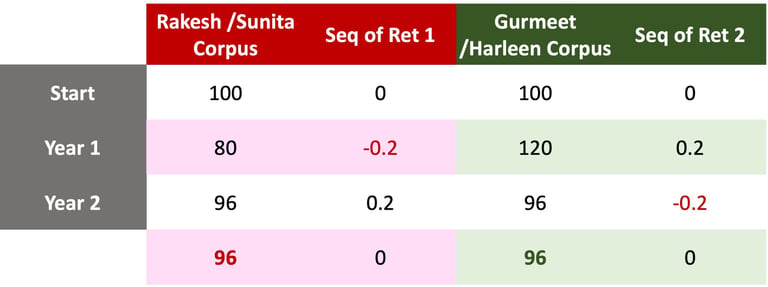

Let’s say Rakesh and Sunita invested Rs. 100 in an Index. The first year they lost 20% but in the second year they gained 20%. At the end of the period, their corpus is Rs. 96 = 100 x (1 - 0.2) x (1 + 0.2) Refer to Table 1. Similarly, Gurmeet and Harleen invest in another Index which gives the same returns, but in reverse. They gain 20% in year one and lose 20% in year 2. At the end of year two they have the same corpus as Rakesh and Sunita, I.e. Rs 96 = 100 x (1 + 0.2) x (1 - 0.2).

Table 1.

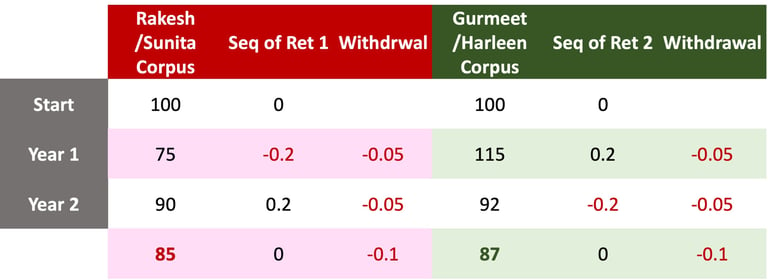

The twist comes in when retirees make these investments to fund their retirement yatra. Being a retiree implies they must withdraw some money every year to run their household. It’s this withdrawal that makes the “Sequence of Returns” so dangerous. Let’s take the above example and add 5% withdrawal to it at the end of each year. Refer to Table 2. As you can see, Rakesh and Sunita, the unfortunate couple got the wrong draw. They lost 20% in the first year and had to withdraw 5%. Despite a 20% gain in the second year, at the end of the 2 years, their corpus has depleted to Rs.85. Gurmeet and Harleen on the other hand who gained 20% in their first year, end the second year with Rs. 87. From here on even if for the rest of the retirement years , both the couples get the same returns, Rakesh and Sunita will progressively fall behind. Or they are at a higher risk of “Portfolio Failure” than Gurmeet and Harleen because their base has shrunk while expenses remain the same.

Table 2.

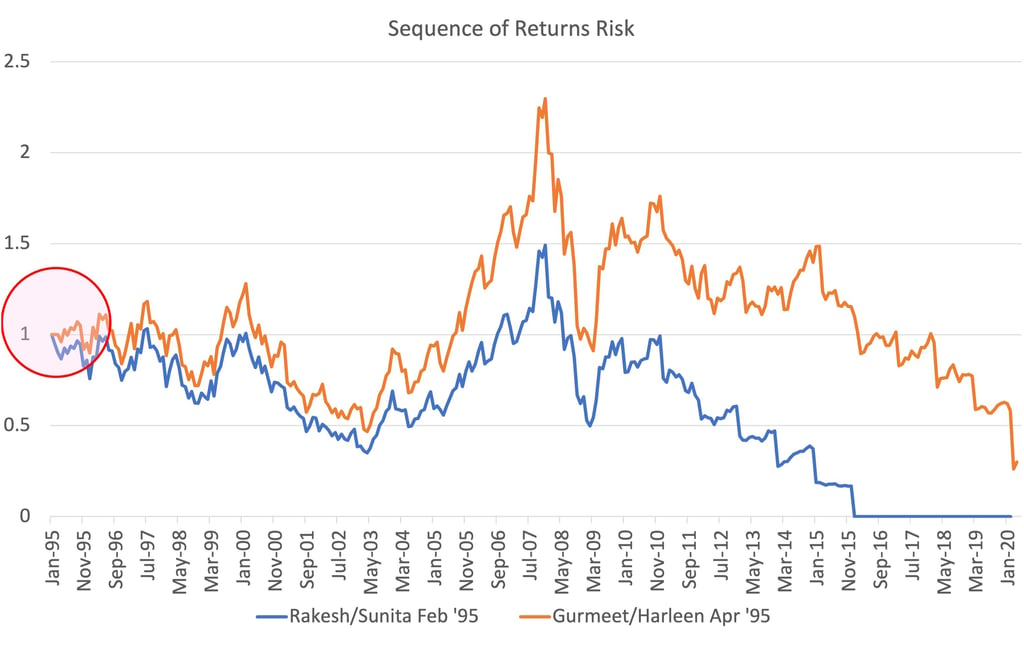

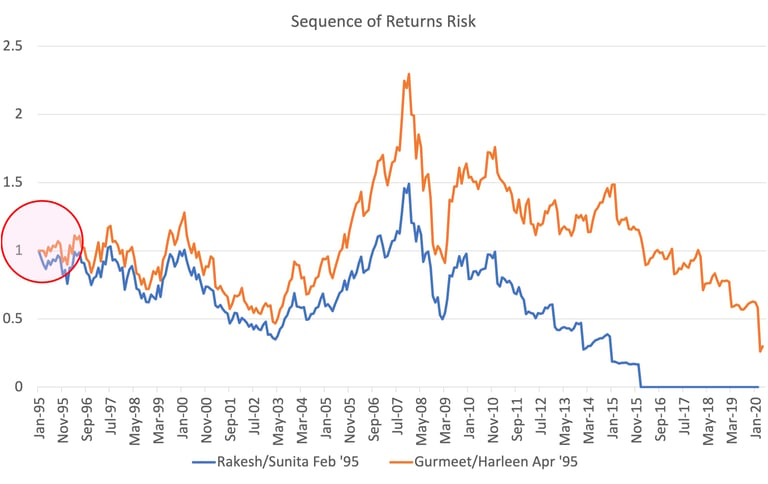

The same can be projected on the real world. Rakesh and Sunita retired in Jan’ 95 and put their life’s savings in Sensex by end of Jan. Gurmeet and Harleen followed them couple of months later in Mar-Apr’95. They both chose 5% Withdrawal Rate (The first year withdrawal as percentage of their starting corpus, adjusted every year based on prevailing inflation). Over the next 25 years, Sensex returns for both the couples were ~10% CAGR. However, the first year returns for Rakesh were negative, -19% (before yearly withdrawal) while for Gurmeet were positive +3%. This is highlighted in Fig. 1. In the second year, Rakesh and Sunita gained 15% while Gurmeet and Harleen stayed the same and yet there was 11% gap in their corpus. All this happened right at the beginning of their Retirement Yatra. As a result while Gurmeet and Harleen made it to Mar '20 with some gas still in the tank(Remember Mar '20 was the worst of Covid) while Rakesh and Sunita, ran out of money post 2016 withdrawal.

Fig 1.

One may ask, if there are ways to protect against such vagaries of SOR. Yes, there are.

The safest alternative is to avoid investing in assets with variability of returns. Go for Govt. Treasuries instead of equities, gold. bonds etc. I’ve covered that here.

The second approach is to create an alternative plan based on Dynamic Withdrawals. I’ve covered that here.

The third alternative is “Bucketing”. Create an emergency fund right at the time of beginning your Retirement Yatra. Fund may have a year or 2 worth of annual expenses. Invest that in the safest of instruments such as FD, Liquid Funds, Arbitrage Funds, Call Money Market funds to name a few. Use that fund to meet expenses in the initial years only if there is serious erosion of corpus in the initial years. I’ve covered Bucketing Strategy here.

There is no way to predict these outcomes in the future. But trailers do foretell what the future may hold. Remember, forewarned is forearmed

Disclaimer : I'm NOT a SEBI Registered Investment Advisor or Analyst. All content on this website is for educational purpose only. Consult your financial advisor before making any financial decision including investing.