1990-2024 Dynamic Withdrawal Plan - III

Introducing Dynamic Withdrawal Plan for retirees. Comparing it with constant Safe Withdrawal Rate. The pros and cons.

Aseem Sharma

7/1/20245 min read

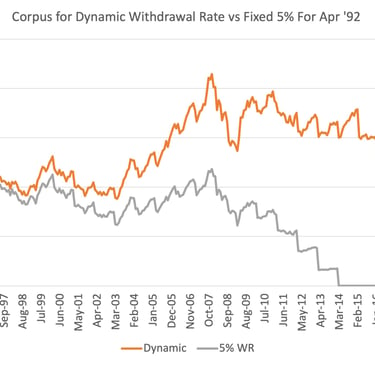

Fig. 1

In Part - I and in Part - II of this series, we looked at different combinations of PPF, SENSEX and Gold for Max Withdrawal Rate. We checked out Portfolio Success for different Withdrawal Rates for different asset allocations. However, for all Retirement Plans, the Withdrawal Rate was fixed right at the start of the plan and stayed the same right through the journey. The only change was adjusting it to inflation every year. While this approach gives us constant buying power right through the Retirement Path, there are times it falters and may cause the retirees financial distress by exposing them to Portfolio Failure.

In this post we look at reducing the risk of “Portfolio Failure” by adopting a plan that helps navigate market gyrations. We explore “Dynamic Withdrawal” approach. The objective is to make the corpus last the entire duration of the plan irrespective of whatever tantrums Ms. Volatility throws. We prioritise Portfolio Longevity over Withdrawal Rate’s constant buying power. To achieve this objective we need to build a little flexibility in our withdrawal rates. Our aspiration would still be to achieve the original withdrawal rate as but be open to cutting withdrawals if there is a serious erosion of corpus. We do all this while keeping the original asset allocation. We are not going to dump equities once they have tanked. We do so because research has shown that majority of the best market up moves come within days of a violent down move. So, we do not want to let panic get the better of us and sell off our investments post a market crash.

The Dynamic Plan

The approach requires us to make 2 withdrawal plans and run them concurrently. At the time of making the annual withdrawal, we compare the two and pick the one that makes sense. The first plan is the original plan with constant Withdrawal Rate. The second plan is based on the Max Withdrawal Rate calculated for the remaining of the tenure. Remember, we calculated the Max withdrawal rate for a range of timeframes in Part - II of this series. The plan is to leverage that insight whenever we make our annual withdrawal. What we are essentially doing is suspending our original plan and strapping on to the safest plan available for the remainder of the duration with whatever corpus we have at the time of making the annual withdrawal.

Let’s go over an example. Let’s say Rakesh and Sunita, our friends from the previous post, started their journey with Rs. 30 lacs of Retirement Corpus in April of ’92 just as Sensex peaked during Harshad Mehta’s glory days. They felt optimistic about their future and went with a 5% withdrawal rate. They invested 50% of the corpus in PPF and the other half in SENSEX. By the time they came around to their first withdrawal, their corpus had already tanked 13% from the time they started off. Taking into account inflation of 6.3%, as per their original plan they should have withdrawn 0.05 x (1 +0.063) = 5.3% of Rs. 30 lacs, except that they also created the dynamic withdrawal plan using Max withdrawal Rates for different timeframes. So they looked up 29 year timeframe and picked up 5% Max Safe Withdrawal Rate. Note that they need to apply this 5% to reduced corpus as this is now their starting corpus for a 29 year journey.

Withdrawal Choices

The constant Withdrawal rate allows them to withdraw 0.053 x 30,00,000 = Rs. 1,60,000. However, they withdrew 0.05 x 0.87 x 30,00,000 = Rs. 1,30,000 as suggested by the dynamic plan. Taking a 20% haircut is tough, but as we will see, such a call eventually paid off.

Every year since, they did this comparison at the time of annual withdrawal. They never really gave up hope of getting back to their original plan, but in favour of financial prudence, they compared between the Max Withdrawal Rate for the remaining duration and the original 5% inflation adjusted Withdrawal Rate and picked lower of the two.

As we trace the two alternate Retirement Paths over the years (Fig. 1 above), we see that by embracing a dynamic withdrawal approach they just about made it through 30 years. Tracking to the original plan and sticking to 5% withdrawal rate leads to them run out of money in 2014, a good 8 years ahead of the planned duration. Refer to Fig 1. for the Retirement Paths.

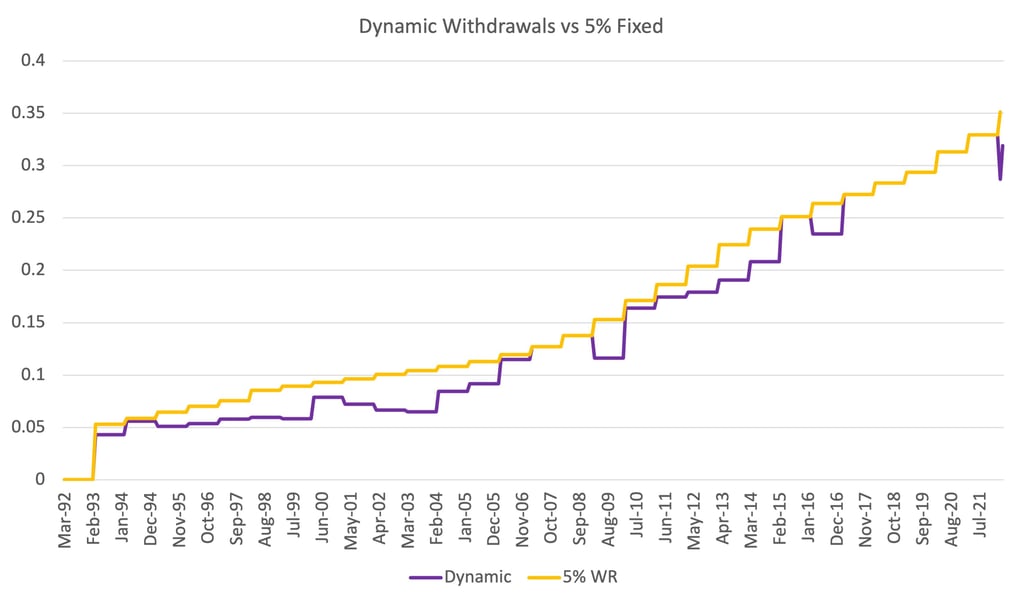

Fig. 2

Let's now look at actual withdrawals along the way. Fig. 2 compares the year on year actual withdrawals between the the fixed 5% plan vs dynamic plan. One would notice, there were many interleaving years where the withdrawals were lower than constant withdrawal rate plan. Those were the tough calls Rakesh and Sunita made to get themselves a longer financial runway. Also, there were times, such as in 2006 and 2007 where they caught up to their original 5% withdrawals. However, the bull run of 2004-2007 was followed by 2008/2009 crisis. Rakesh and Sunita again had to fail over to dynamic withdrawals until the last 5 years. We do not have a Max withdrawal rate for 1 - 5 years. So we follow the constant withdrawal rate 5% adjusted to inflation from 25-30 years.

This need not be the journey for every retiree. In fact Apr ’92 was the worst time to start retirement in the history of SENSEX. We discussed in an earlier post that Retirement Plans are most vulnerable to market downturns during early phase of retirement. It's called Sequence of Returns (SOR) risk. If one has a few good years of returns early on in their journey, they build up a natural buffer against future downturns. But this can’t be predicted in advance, hence keeping your minds open to a dynamic withdrawal plan can help you survive temperamental Ms. Volatility.

Retirees may be okay to temporary cuts but ideally one would like to get back to the lifestyle one is used to, i.e. finances permitting. Dynamic Plan could help there as well. Dynamic plan is not just for slashing withdrawals, it works equally well on the other side of the retirement curve too. Dynamic plan could also unlock higher withdrawals using the same principles.

For example, Lets paint an alternate scenario for Rakesh and Sunita. Assume the the first year of retirement was a good one. The corpus grew by 12%. The starting corpus of 30 lacs became (1 + 0.12) x 30,00,000 = Rs. 33,60,000. The constant 5% Withdrawal Rate adjusted to inflation comes to 5.3% . At the time of the first withdrawal going by constant WR they would withdraw 0.53 x 30,00,000 = Rs. 1,60,000. On the other hand, applying Dynamic withdrawal rate of 5% we get 0.05 x 33,60,000 = Rs. 1,68,000. As 5% is a Safe Withdrawal Rate for 29 years, Rakesh and Sunita can give themselves a raise of Rs. 8000 without worrying about Portfolio Failure and move up the withdrawal ladder.

In summary a Dynamic Withdrawal Plan(DWP) is a plan with pre-set guardrails. These guardrails ensure that the Retirement Plan never veers off course. Basing the Retirement plan on DWP, may allow retirees cruise without the fear of Portfolio Failure.

Research shows, in most retirement plans the retiree finally ends up with a large corpus at the end of the journey, a corpus larger than the one she started off with. A dynamic plan enables one to enjoy part of their growing corpus in their living years. All it needs is the retiree to commit to lowering withdrawals during market downturns. In most cases these these cutbacks will be temporary allowing them to scale back up in time.

Disclaimer : I'm NOT a SEBI Registered Investment Advisor or Analyst. All content on this website is for educational purpose only. Consult your financial advisor before making any financial decision including investing.